The mass customization of banking services

Discover how generative artificial intelligence is transforming banking in Latam, enabling mass personalization without losing efficiency. Insights, challenges and real cases presented by Delto at Fintech Americas 2025.

.avif)

Facundo del Pino, Director of Operations

At the event Fintech Americas 2025 in Miami I had to give a presentation with Hector Deambrosi, Head of Sales of Infocorp for Latam, on the opportunities that the implementation of Generative Artificial Intelligence in banking It offers for massively customize the customer experience.

In this article I would like to share the content of our talk, some reflections and applied cases on this crucial topic for digital banking transformation.

Generative artificial intelligence challenging paradigms

The title of our presentation, proposed by the event's organization, was “Tailor-made: The Rise of Mass Personalization”, and aimed to demonstrate how in Delto we achieved this effect through the integration of Gen AI In the banking channels.

At first glance, the title seems ironic, we are used to the fact that the personalized and the massive are opposites, and in most of the cases that may come to mind they are indeed opposites. However, the Generative AI has one of its great differentials in being able to provide a highly personalized experience for each individual but in a way scalable.

Before looking at concrete examples, let's put both concepts in the context of banking in Latin America:

Bank users (as well as other institutions) under the umbrella of personalization are looking for:

- Relevance and timing: that the interactions are what they need and when they need them.

- 24/7 availability: be available around the clock.

- Context and memory: that technology identifies who the user is and remembers what they talked about before.

- Immediate solution: they want clear guidelines when it comes to whether what they want is resolved or when it is going to be resolved.

Banks, on the other hand, under the umbrella of the mass, seek to:

- Increase revenue: reach more customers with more products

- Improve customer experience: Improve the quality of interaction by offering more channels with high standards of service and convenience as well as convenience.

- Operational cost efficiency: that the number of interactions is not linear to the cost of performing them.

- Scalability: Quickly replicate models that work without major friction.

Previously, these worlds seemed to be opposites, often even divided into dissociated units of care, some more popular and others more premium.

With the arrival of the generative artificial intelligence, this paradigm is beginning to be questioned and very interesting possibilities are opening up for banks to improve the quality of customer experience at a “premium for all” level, maintaining or even reducing operating costs. Let's look at some numbers and examples that support this transformation in the banking industry.

The impact of Gen AI on banking according to consulting firms

Once we understand the potential of Generative AI as a link between personalization and mass, it's quite intuitive to accept these promises of benefits, but it's always convenient to back up with numbers.

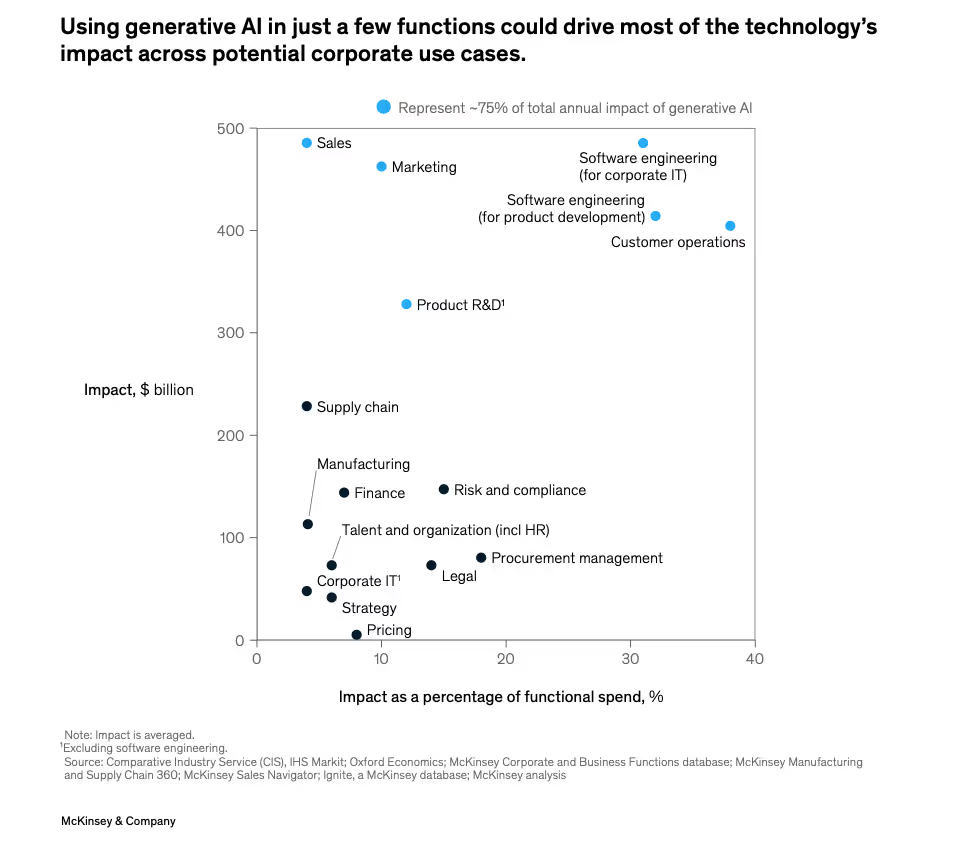

Analyzing different sources and reports made by renowned consulting firms, we can conclude some extremely interesting insights. In short, they not only indicate that the implementation of conversational channels in Customer Operations (both customer service activities) as transactional with the end customer (such as transfers, insurance contracts, credit card transactions, among others) has a tremendous impact potential, but also the banking industry in itself, it is the second industry with the greatest potential to receive benefits.

Summary of some key indicators:

- Marketing, sales and customer operations (all customer-facing activities) are among the 6 activities with the highest potential for impact, representing 75% of the total projected benefits.

- Customer Operation is the area with the greatest potential benefits in terms of operational efficiency with almost 40%, that is, in other words, what a company could save in costs for this activity by incorporating GenAI.

Making the cut by sector, as mentioned above, we can find the following for the banking industry:

- Banking is in second place in the order of potential impact by industry.

- The expected economic reach is between 2.6% and 4.7% of the industry's total revenue, which for banks is between 200 and 340 trillion dollars.

- The areas with the greatest expected impact within banking are: customer operations, marketing and sales, software and compliance.

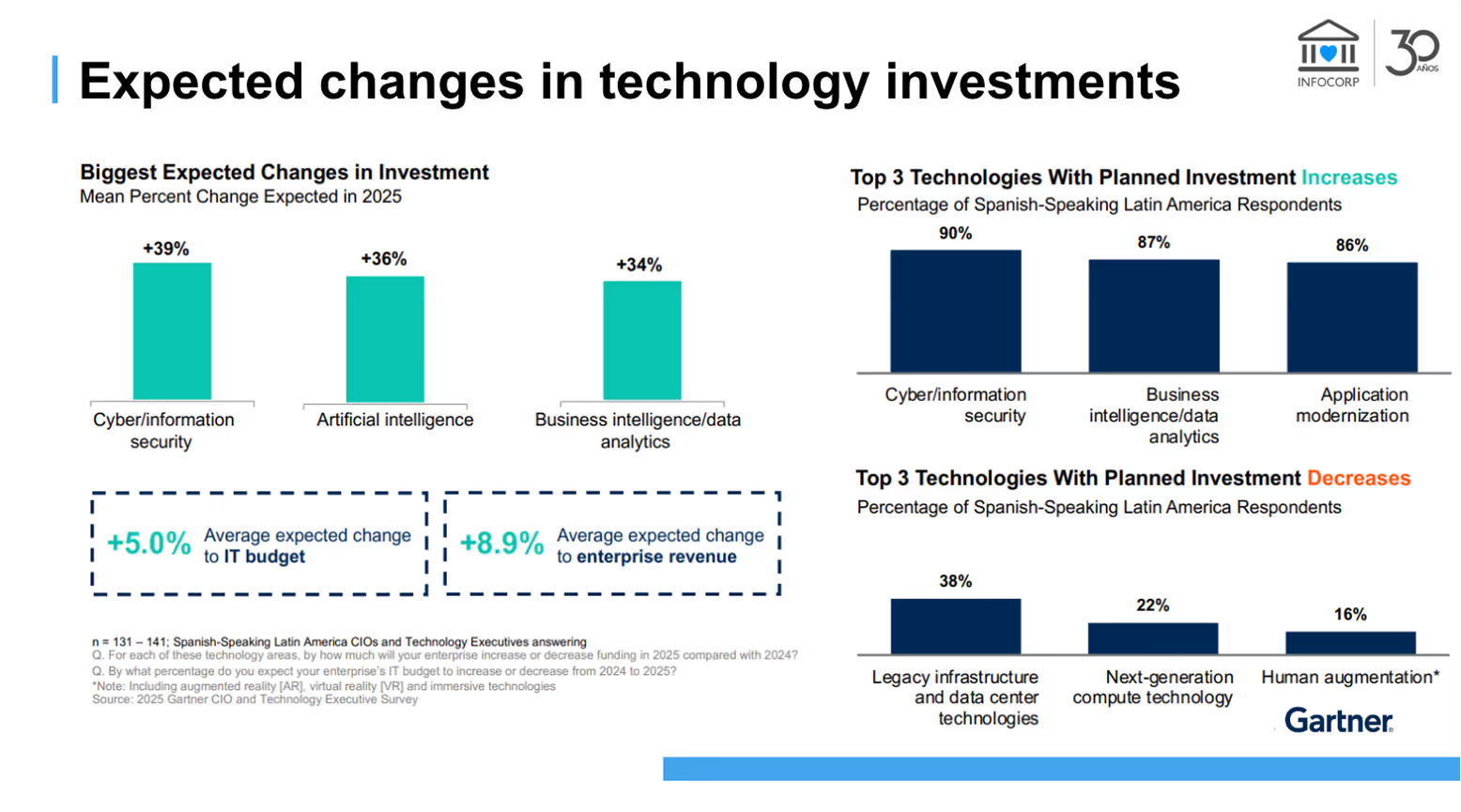

In addition to these potential indicators, we also found that the investment intention of decision makers is aimed at increasing investment in GenAI In the banking sector.

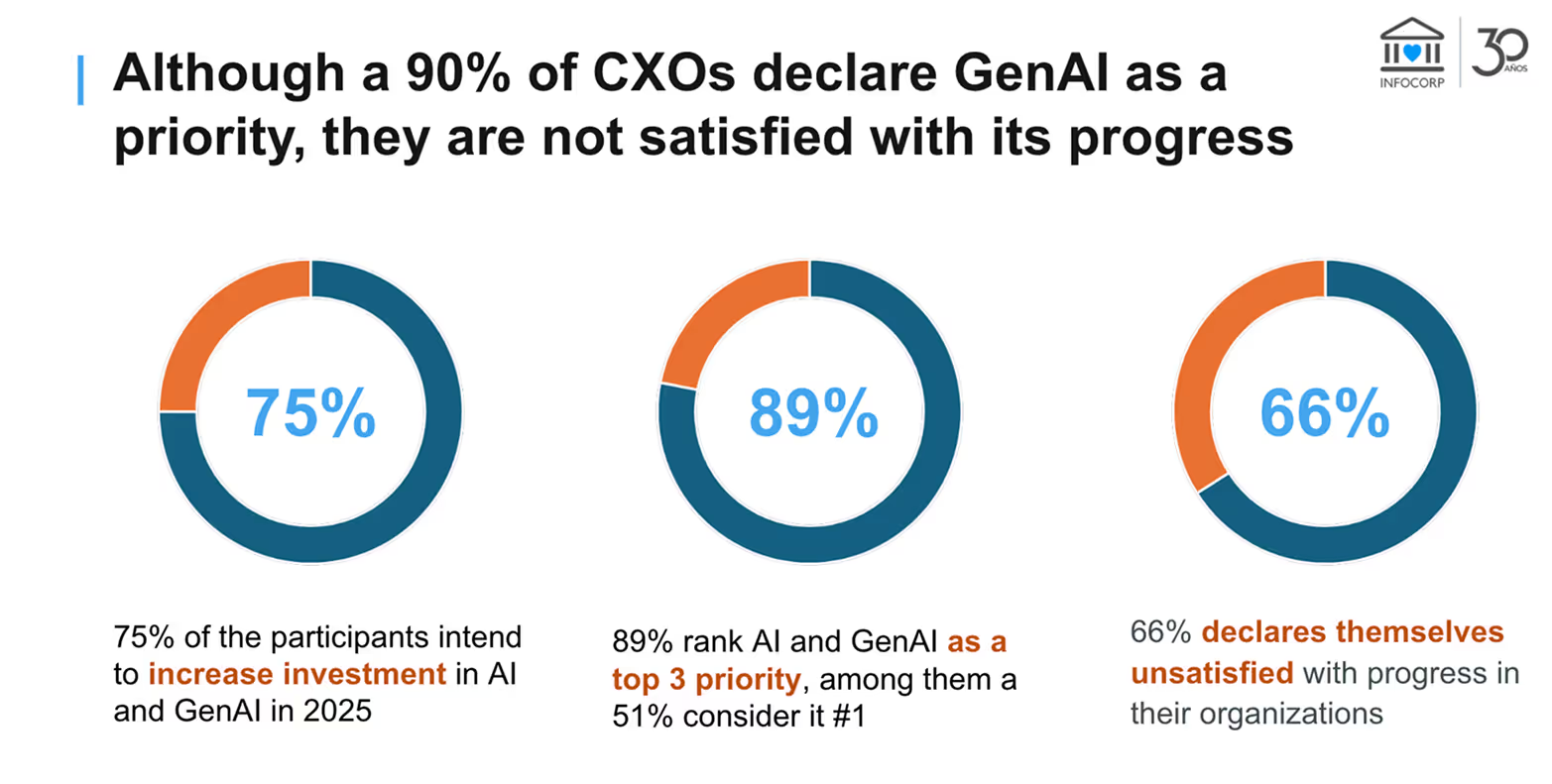

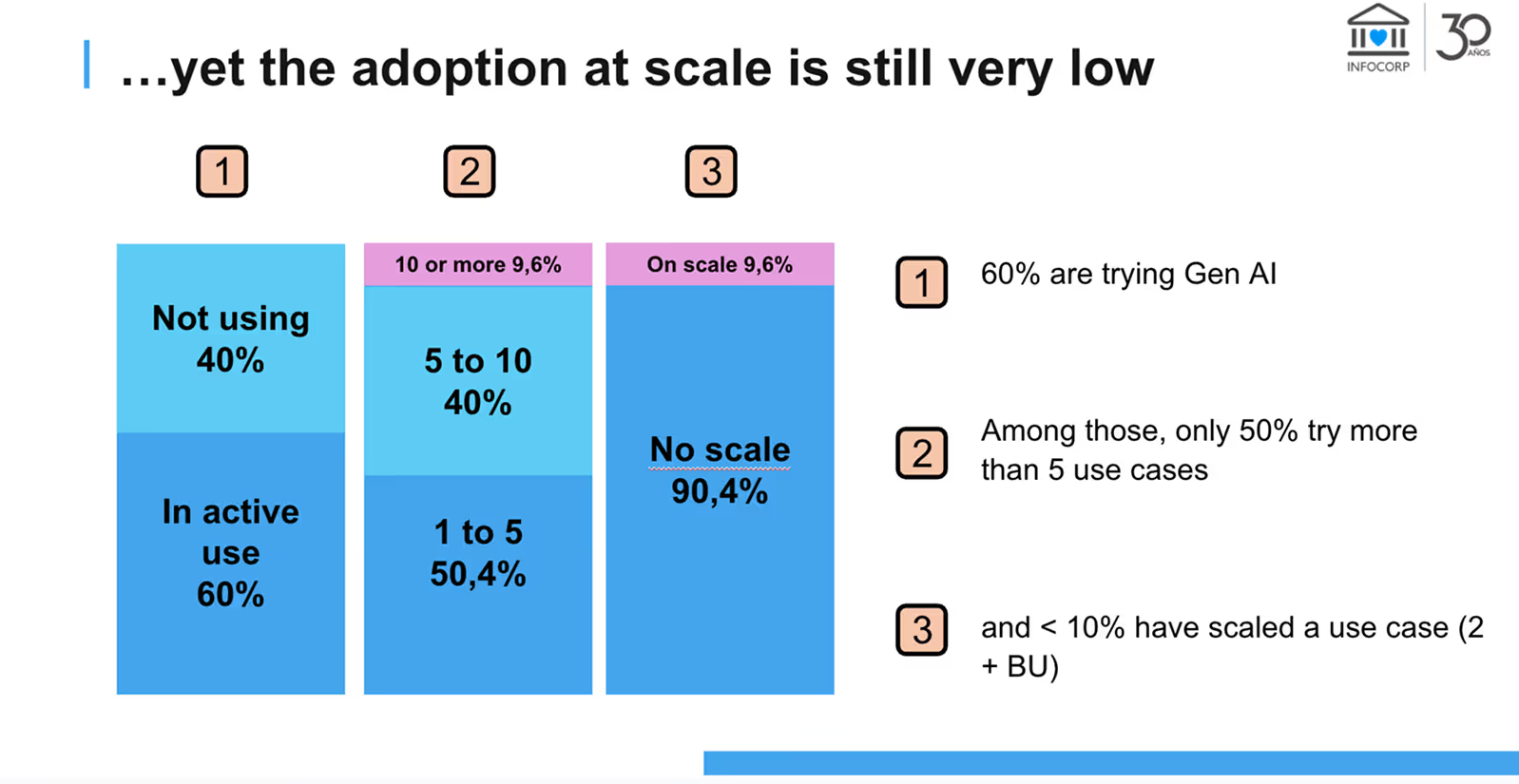

However, beyond the predictions of high benefits and the explicit intention to invest in them, the decision makers themselves are not satisfied with the results obtained and are finding it difficult to find sufficient arguments to expand the implementation beyond a couple of use cases.

Challenges in implementing Generative Artificial Intelligence in banks

In our opinion, we can partly explain this dissociation between potential and reality by a normal process experienced in most technological disruptions. To put it in a simplified way, we are at a time when, after the initial hype, we are realizing that in order to take advantage of the potential of Chatbots in banking, significant work, precautions and adjustments are required. In other words, incorporate Gen AI to business processes, and even more so to the banking industry, is not as easy as it seems or sometimes we are told; but the positive thing is that it is possible.

Some of the most common challenges we face when implementing this type of technology are the following:

- Hallucination control and precise segmentation of the capabilities of conversational agents.

- Efficient and scalable use of tokens and management of the costs associated with LLMs.

- Modular and iterative growth of conversational agents for quick results and building trust.

- Infrastructure, security and governance of data and potential sensitive information

- Compliance with specific banking industry regulations (central banks and superintendencies) nationally and internationally, both current and future.

These challenges are real concerns and challenges for financial institutions seeking to implement this type of technology in different banking business units. Specifically, those points are the pains that we seek to resolve in Delto with our product, offering robust and secure conversational solutions for banking. If you want to know more about how we can help you, you can visit our solutions page.

But as we mentioned above, these types of challenges, obviously with the peculiarities of the case in question, are part of the normal process of learning and technological innovation. In this case, it is key not to lose sight of the potential benefit it offers and the good practices necessary to overcome the various obstacles.

Examples applied to banking in Colombia and Argentina

Below, we share some examples that we presented at Fintech Americas 2025 and that we are currently implementing in Delto with different customers to improve the customer experience. These are merely representative examples of some capabilities applied to some use cases, but as a reference currently in our product we have more than 300 capacities (we call them skills) pre-designed for banking, most of them have the capacity to perform actions similar to these in different use cases, both customer service and transactional, including transfers, payment for services, etc.

Conclusions

We closed the talk with some insights that I share below, where we present some conclusions that are far from revealing, but rather common sense, but which, being of this type, also allow us to see the implementation of projects of generative artificial intelligence in banking much closer and more palpable.

What we highlighted was:

- La Gen AI has the capacity to be the link between two “worlds” that seemed to be at odds, personalization and massiveness.

- The potential impact of this technology is real and very significant, especially for Customer Operations Within the banking industry within Latin America.

- There is a clear intention to implement this type of technology in the banking industry and the ability to access investment to do so.

- It is important to know all the challenges that will be presented to us along the way and that technology itself is not the only thing to consider.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------

In Delto we specialize in the implementation of conversational channels with generative artificial intelligence for the banking industry. If you're interested in learning more about our solution and how we can help you transform your customer experience, don't hesitate to contact us.

En Delto nos especializamos en la implementación de canales conversacionales con inteligencia artificial generativa para la industria bancaria. Si estás interesado en conocer más sobre nuestra solución y cómo podemos ayudarte a transformar la experiencia de tus clientes, no dudes en contactarnos.